DebtFree

Pay off debt faster — without linking your bank.

Pay off credit cards, loans & medical debt faster with the Snowball and Avalanche methods and a live debt-free date. No bank logins. No subscription.

DebtFree

finance

Pay off debt faster — without linking your bank

Account

Not required

Analytics

Opt-in & anonymous

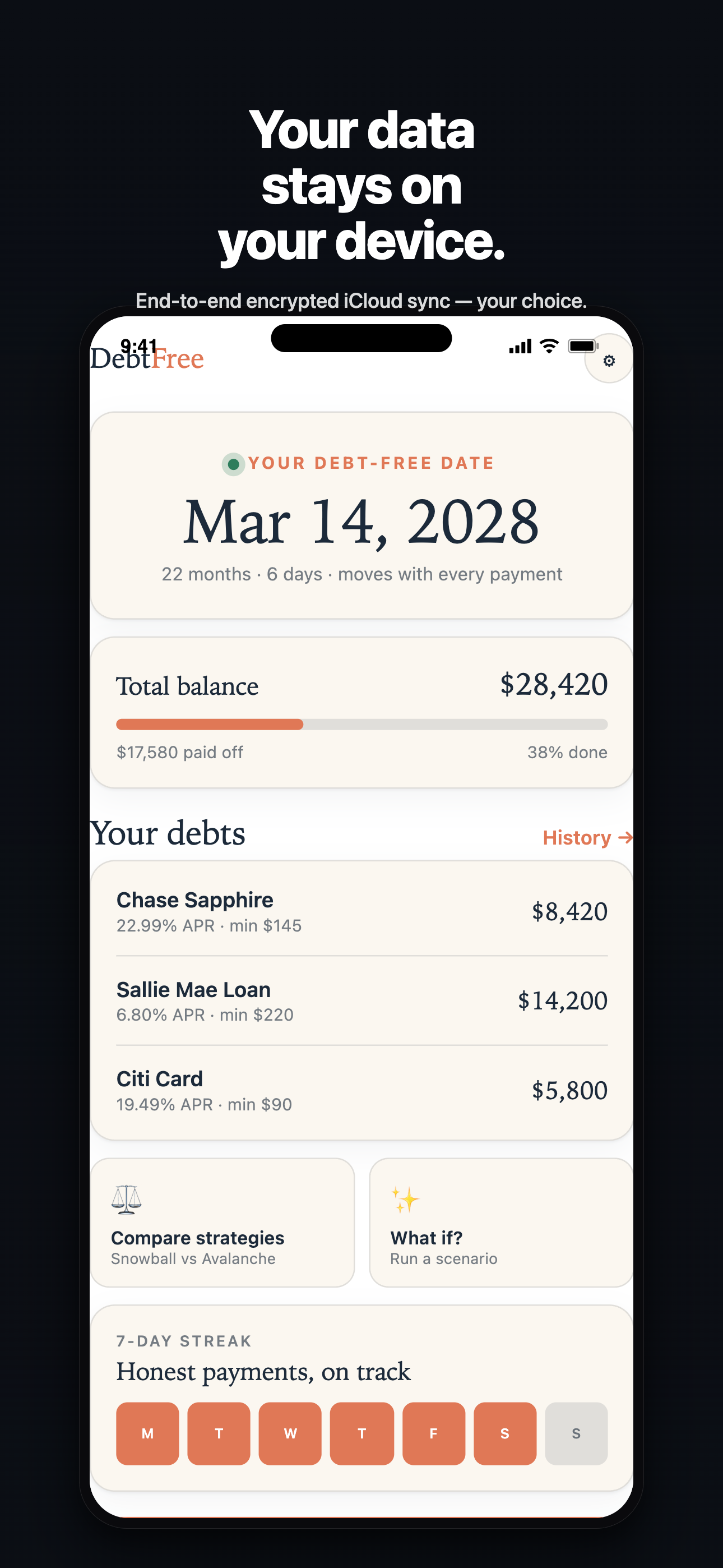

Your data

Stays on device

Ads & trackers

Zero

What you get

Built for exactly this — and nothing you don't need.

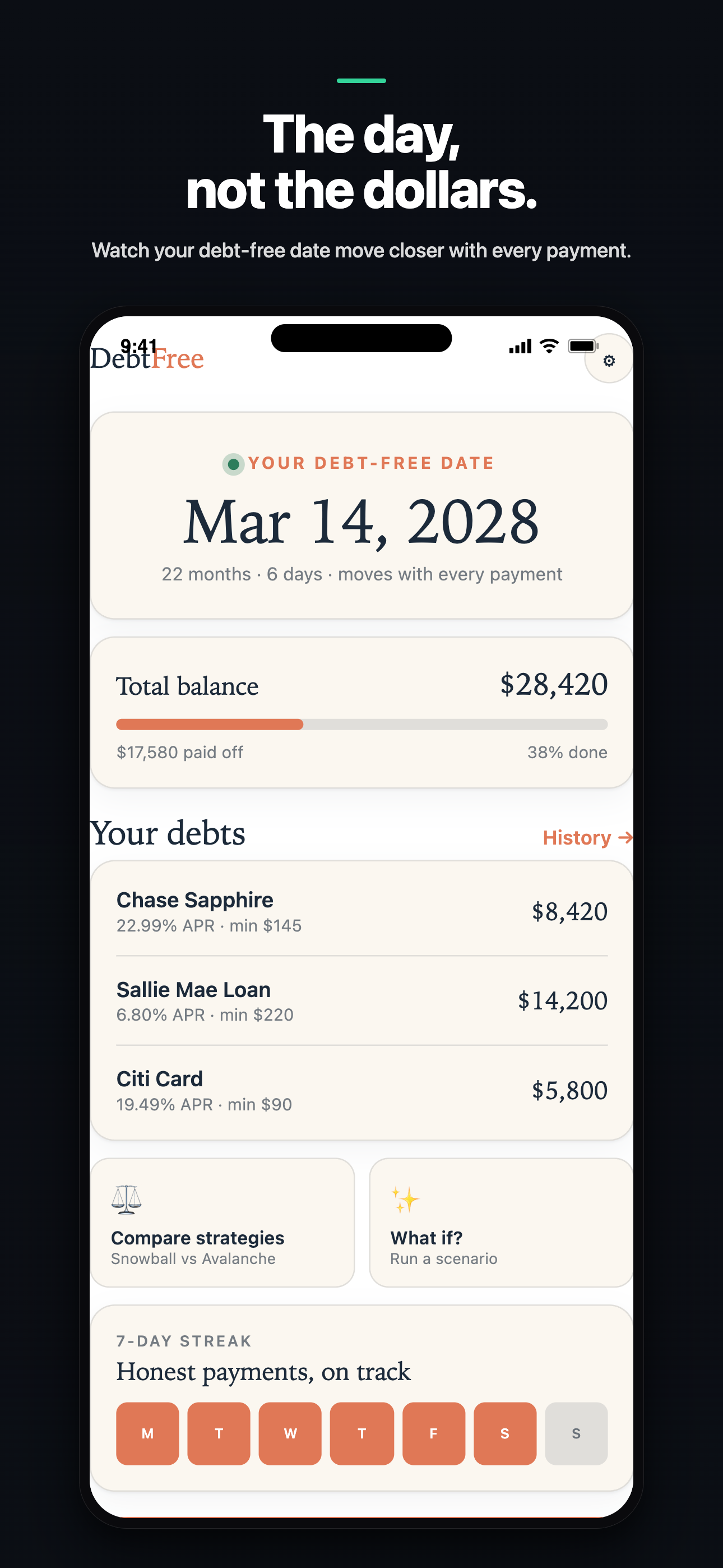

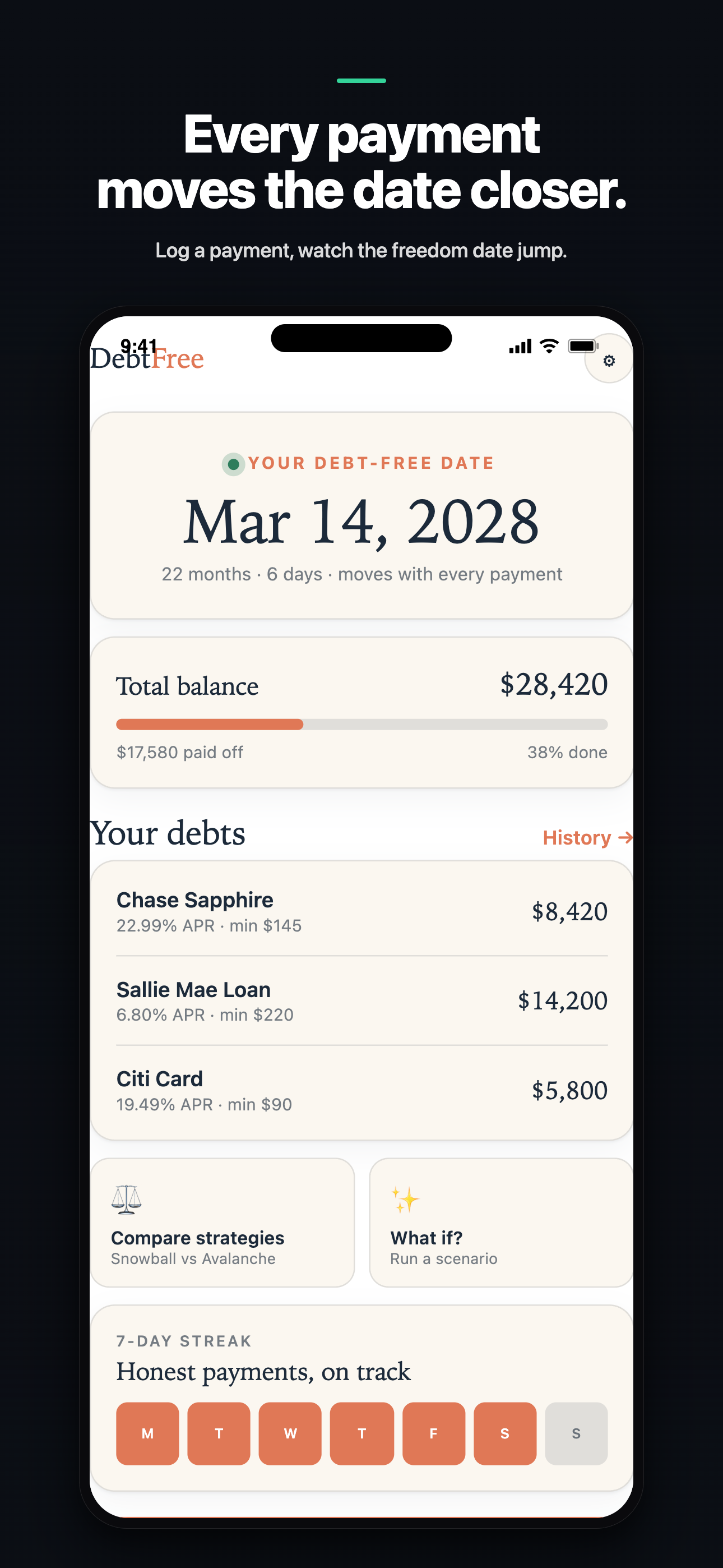

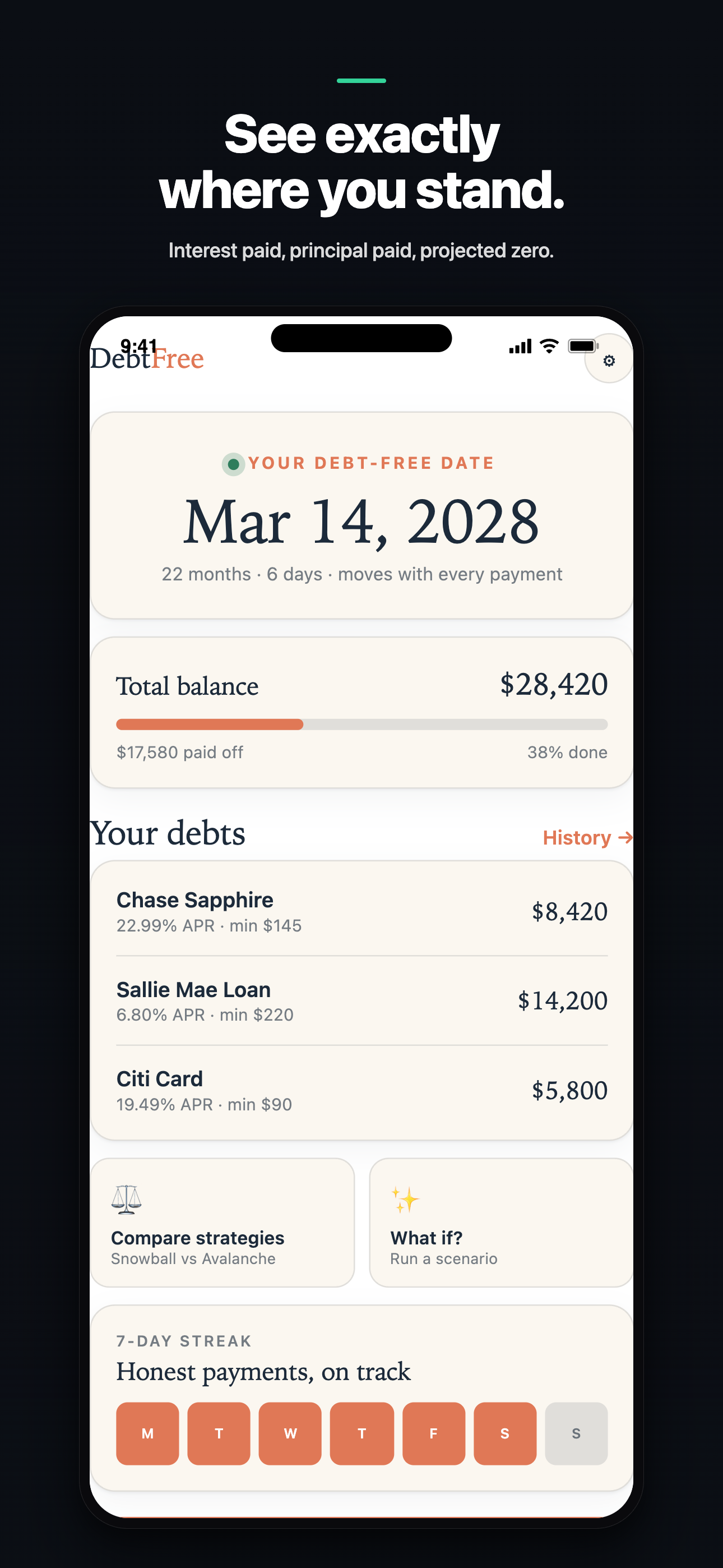

Watch your debt-free date move closer every time you pay

a live payoff projection that turns "someday" into a real date on the calendar.

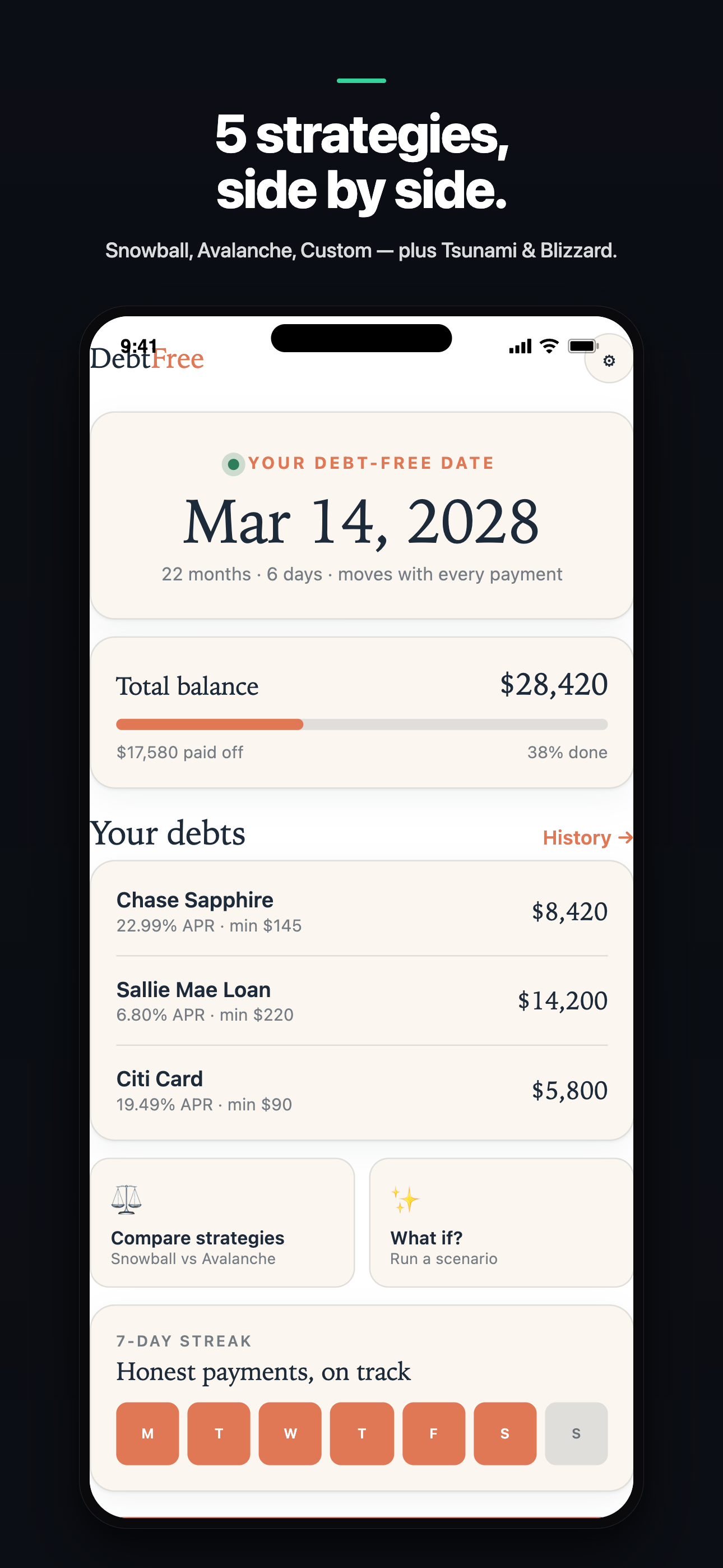

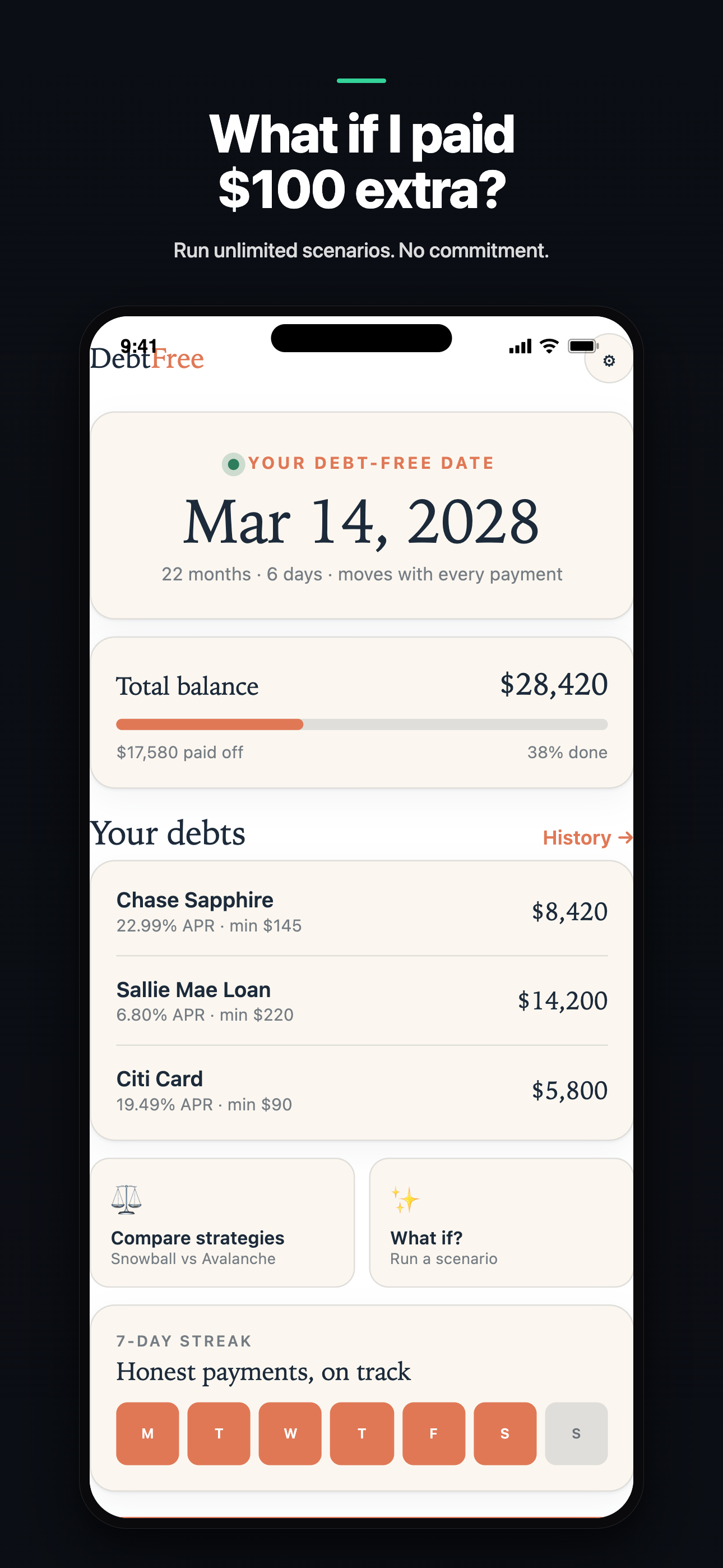

Pay off debt faster with five strategies

Snowball (smallest balance first), Avalanche (highest APR first), Custom order you control, plus the DebtFree-original Tsunami and Blizzard.

See exactly what one extra payment buys you with the What-If simulator

how many months sooner you go debt-free and how much interest you save.

Track everything you owe in one place

credit cards, student loans, medical bills, auto, mortgage, and personal loans: 12 debt types across 15 currencies.

Read your whole plan at a glance with a month-by-month payoff calendar that maps every balance all the way to zero.

Stay motivated with the DebtFree Score, a private 0–1000 momentum gauge (not a credit score), plus milestones for your first payment, the halfway mark, and every debt destroyed.

Pay down household debt together with Couples mode

merge two debt stacks into one shared freedom date so partners get there as a team.

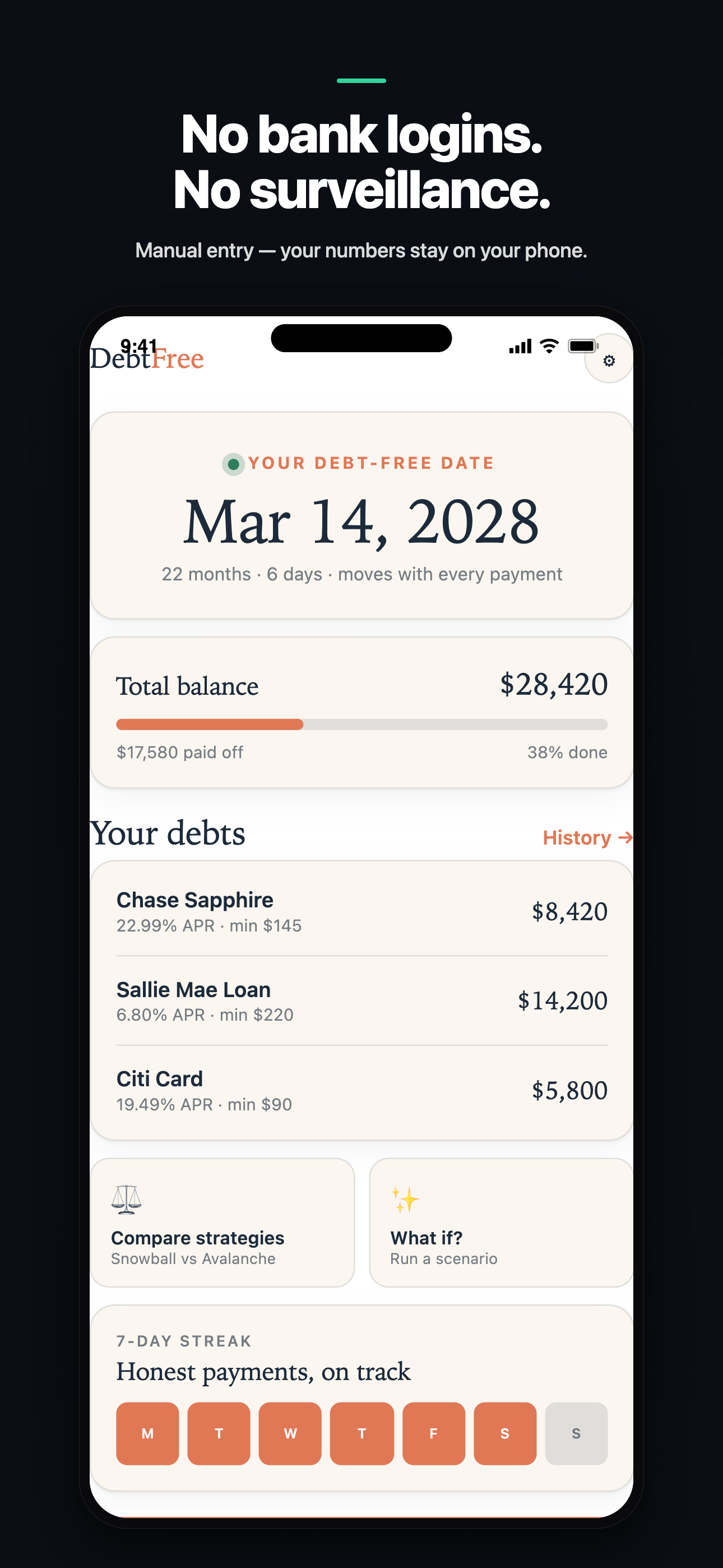

Private by design

no bank linking, no account, no sign-up. Balances stay encrypted on your device with an optional Face ID / biometric lock and a passphrase-protected backup you control.

A look inside

See it in your hands.

How it works

Up and running in under two minutes.

- 01

Add your debts

Enter each balance, interest rate, and minimum payment. Takes about two minutes — no bank login required.

- 02

Pick your strategy

Snowball, Avalanche, Custom, Tsunami, or Blizzard. See your payoff plan recompute instantly.

- 03

Watch your freedom date move

Every payment recalculates the date. The what-if simulator shows what one extra payment really buys you.

A note from the studio

“I built DebtFree after watching people I love white-knuckle their way through credit-card and medical debt — and then get told to hand a budgeting app their bank login on top of it. Debt is stressful enough without a monthly subscription or a company quietly watching every transaction. So I made the tracker I wished they had: you pay once, you never link an account, and the only thing it follows is your progress toward a debt-free date you can finally see.”

Questions

The honest answers.

Do I have to connect my bank?

No — and you can't. DebtFree never links to a bank or credit card account. You enter your balances yourself, so nothing sensitive ever leaves your phone. There's no Plaid, no bank login, and no syncing your transactions.

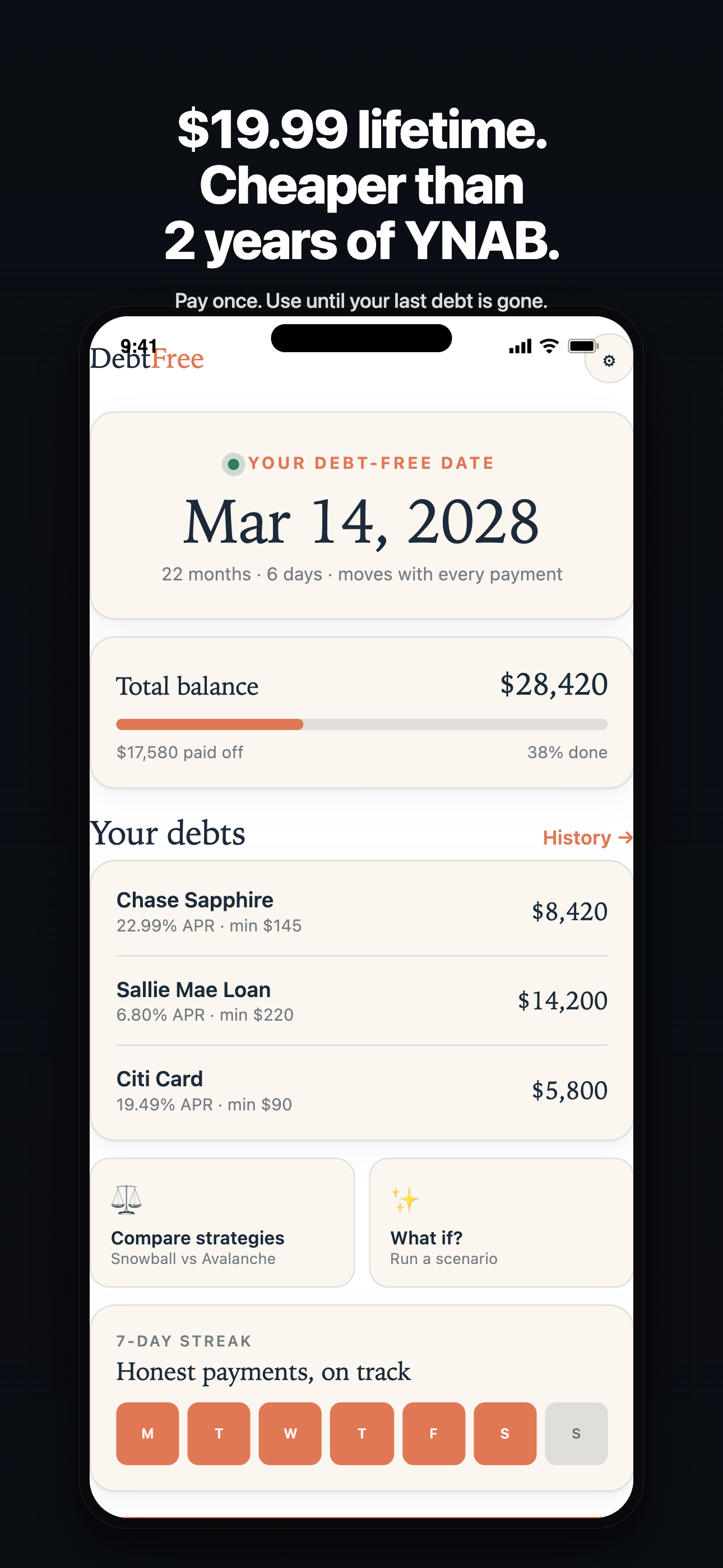

Is it a subscription, or a one-time price?

One-time. DebtFree Plus is a single $19.99 lifetime unlock (₹1,499 in India) — no monthly or yearly fee, ever. Couples mode is a separate one-time $29.99 add-on. Debt is stressful enough without another recurring bill.

Is there a free version?

Yes. You can track up to 2 debts for free with a real payoff projection and your live debt-free date. Upgrading to Plus unlocks all five payoff strategies, the What-If simulator, the full payoff calendar, and more — as a one-time purchase.

Does it work offline?

Completely. DebtFree runs fully offline and needs no account. The only network call is to the App Store to validate your one-time purchase — your debts, balances, and payment history never touch a server.

Do you show ads or sell my data?

Never. No ads, no data sale. Optional product analytics and crash reports are off by default, and even when you turn them on they never include your balances or lender names.

How is this different from YNAB, Rocket Money, or a budget app?

Budget apps want your bank login and a monthly subscription. DebtFree does one thing — get you out of debt — with zero bank linking, a one-time price, and a single freedom date that moves with every payment. It's a focused debt payoff tracker, not a full budgeting platform.

What is the DebtFree Score?

A private 0–1000 gauge of your payoff momentum, built from your progress, interest saved, streaks, and on-time payments. It is not a credit score and has nothing to do with FICO or your lenders — it just shows you're moving in the right direction.

What platform is it on, and is it really financial advice?

DebtFree is built for iPhone and available on the App Store. It's a self-directed planning and tracking tool — it doesn't provide financial, tax, or legal advice. For that, talk to a qualified professional.

Launching soon

Be first to know when DebtFree ships.

It'll launch at Pay once — lifetime. Free tier: track up to 2 debts with the snowball method and a basic payoff projection.

One email when it lands on the store. No drip sequence, no spam.

No spam. No tracking. Email only — unsubscribe with one click.

Your debts, balances, and payment history are stored locally on your device (MMKV preferences plus an on-device SQLite database). There is no server copy.

From the journal

Notes on the debt-free journey.

- 01

Why Minimum Payments Keep You in Debt — and the Number Quietly Working Against You

Why minimum payments keep you in debt: the anchoring effect on your statement quietly pulls your payment down. Here's the psychology, and how to take that number back.

2026-06-11

7 min read

- 02

Staying Motivated Through the Long Middle of Debt Payoff

Staying motivated paying off debt is hardest in the middle, after the first win and before the finish. Here's the psychology of the messy middle and how to ride it.

2026-06-11

7 min read

- 03

How to Pay Off Credit Card Debt When the Interest Keeps Outrunning You

Learning how to pay off credit card debt means beating the minimum-payment trap. Here's why high-APR balances feel un-killable, and the order that breaks them.

2026-06-08

7 min read

- 04

How to Get Out of Debt: A Calm Beginner's Guide

A beginner's guide on how to get out of debt — what APR and minimums really mean, how payoff order works, and the first steps that turn dread into a plan.

2026-06-03

7 min read

- 05

Why Most Debt Payoff Plans Quietly Fail by March

Most debt payoff plans fail not from a lack of effort but from how they're built. Here are the structural flaws that doom a plan — and how to build one that holds.

2026-05-29

7 min read

- 06

Mental Accounting and Why Your Debt Feels Bigger Than It Is

Mental accounting in debt is why scattered balances feel heavier than one total. Understanding how the mind buckets money is the first step to thinking clearly.

2026-05-24

7 min read

- 07

Should You Pay Off Debt or Save First? The Question Is Wrong

Should you pay off debt or save first? The all-or-nothing framing trips people up. Here's the small-buffer logic that keeps a payoff plan from collapsing.

2026-05-19

7 min read

- 08

Debt Snowball vs Avalanche: How to Actually Choose Between Them

The debt snowball vs avalanche question is usually answered with math. But the right method depends on your temperament — here's how to decide which fits you.

2026-05-13

7 min read

- 09

How to Pay Off Multiple Debts at Once Without Losing the Thread

Wondering how to pay off multiple debts without spreading yourself thin? There's one mechanism underneath every method — the rolling payment. Here's how it works.

2026-05-07

7 min read

- 10

Debt Avoidance: Why You Keep Closing the App Before It Loads

Debt avoidance is not laziness — it's your brain protecting you from a number it doesn't know how to hold. Here's what actually breaks the loop.

2026-04-26

6 min read

- 11

How to Pay Off Debt Without the Anxiety That Keeps You Avoidant

Most people don't fail at debt payoff because they lack discipline — the anxiety wins first. Here's how to pay off debt without anxiety driving you back to avoidance.

2026-04-08

5 min read

- 12

Your Debt Freedom Date: The One Number That Actually Matters

When you're paying off debt, most people watch the wrong numbers. Your debt freedom date — the day your last balance hits zero — is the only one worth tracking.

2026-03-21

4 min read